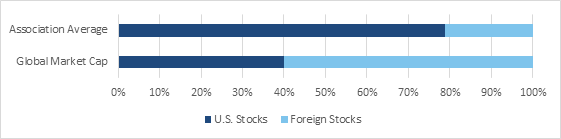

A typical association portfolio allocates less than a quarter of its equity investments to foreign stocks. Should you consider a different approach?

Approximately 60 percent of the world’s publicly traded companies are based outside the U.S. Yet many association investment portfolios look very little like the overall global equity market. According to the ASAE Foundation’s latest edition of Association Investment Policies, Practices, and Performance, the typical association heavily favors U.S. stocks, allocating less than a quarter of its equity investments to foreign stocks.

Source: ASAE Foundation, Association Investment Policies, Practices, and Performance, 2017

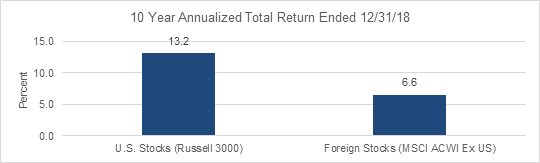

There is a body of behavioral finance research that suggests that home-country bias—the idea that investors inherently favor investments in their own country—is a real phenomenon. Associations appear to be no different in this regard. However, perhaps more important has been the significant dominance of U.S. stocks over foreign stocks measured by performance over the past decade.

Source: Bloomberg

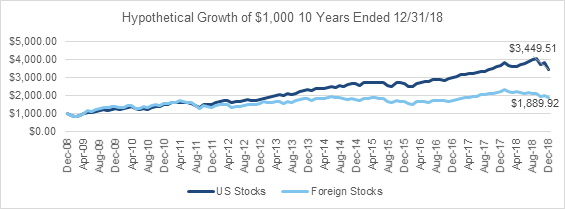

Put another way, $1,000 invested 10 years ago in the U.S. equity market would be worth nearly twice as much ($3,450) as an identical investment in the foreign equity markets ($1,890). This large performance disparity can reinforce the home-country bias of even the most sophisticated investors.

Source: DiMeo Schneider & Associates / Morningstar

Given the magnitude of the performance gap, association investment committees and boards understandably may ask themselves a simple question about foreign stocks: Why bother? But there are three reasons why you may want to increase your foreign stock allocations.

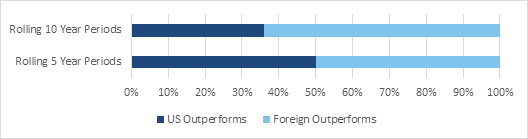

Foreign stocks could outperform U.S. stocks over the next decade. The outperformance of U.S. stocks over the past 10 years can help feed another common behavioral bias, recency bias, whereby we tend to place a disproportionate emphasis on what has happened in the recent past when making future decisions. This phenomenon makes it easy to forget that the relationship between U.S. stocks and foreign stocks has tended to be cyclical and that there have been periods when foreign stocks outperformed U.S. stocks.

In fact, over the past 20 years, the U.S. markets have underperformed the foreign markets over rolling five- and 10-year periods half the time or more.

Source: Morningstar returns and Bloomberg dollar data as of September 30, 2018

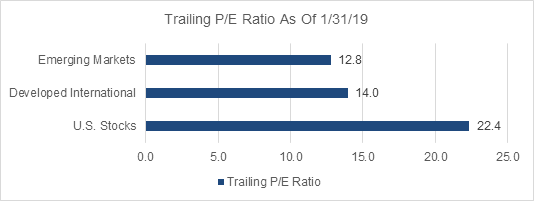

Could the tide be ready to turn back in favor of foreign stocks? No one knows for certain, but as measured by current price-to-earnings ratios, foreign stocks certainly appear cheaper than some U.S. stocks at this point in the market’s cycle.

Source: MSC,I Inc., and S&P Dow Jones

In an increasingly global economy, an investor’s goal should be to identify the best investment opportunities irrespective of borders.

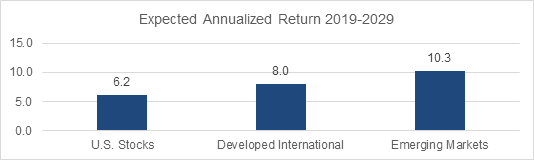

As a result, some firms are projecting meaningfully higher returns over the next 10 years for foreign stocks, especially those in emerging markets, such as Latin America and Southeast Asia.

Source: DiMeo Schneider & Associates, LLC, 10-Year Capital Market Forecasts (2019-2028).

Foreign stocks expand your investment opportunity set. In 2018, the five best-selling cars in the U.S. were foreign made. Seven of the eight largest manufacturers of televisions worldwide, by 2018 market share, were foreign. Even Ben & Jerry’s, an iconic American brand, has been owned by the British-Dutch conglomerate Unilever for almost two decades.

In an increasingly global economy, an investor’s goal should be to identify the best investment opportunities irrespective of borders.

Foreign stocks increase portfolio diversification. Foreign-stock skeptics often argue that large U.S. multinationals that have significant revenues derived from overseas (Coca-Cola is a classic example) provide diversification benefits of foreign investing without the headaches of political risk and currency fluctuation associated with foreign investing. This rationale is potentially flawed for two reasons. First, U.S. multinationals track, as measured by correlation, far more closely their home market than they do foreign markets. Therefore, if foreign stocks outperform U.S. stocks, a portfolio of U.S. multinationals will not fully participate in that growth. Second, sector distribution is not uniform across countries. In the U.S., the information technology and healthcare sectors are dominant, while outside the country, financials and industrials are the largest sectors [PDF].

As with any asset class, associations should carefully examine their allocations to foreign stocks in the context of their time horizon and their ability to tolerate investment risk. Doing so should provide for a thoughtfully constructed investment strategy designed to meet long-range investment objectives.

The content of this article has been obtained from a variety of sources that are believed, though not guaranteed, to be accurate. Opinions expressed do not necessarily represent the views of DiMeo Schneider & Associates, LLC. The content does not represent a specific investment recommendation. Please consult with your advisor, attorney, and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance.