Paul Grambsch

Paul Grambsch is a vice president of wealth management and an institutional consultant at Raymond James in Bethesda, Maryland.

For decades, the 60/40 balanced portfolio has been a mainstay among institutional investors. As the world adjusts to a new normal after coronavirus, it’s time for associations to consider whether they need a new normal for their investment portfolios.

The global pandemic has challenged long-standing assumptions held by many associations, forcing some to adapt their business models and diversify revenue streams. Those fortunate enough to have strong investment reserves have been able to tap into their “rainy day funds” to maintain business continuity as they adapt their organizations business model to the “new normal.”

Business models aren’t the only models that have been challenged by the pandemic. The long-standing assumptions underlying the very 60/40 balanced portfolio model used by many reserve funds may also need to be challenged. That 60/40 model is a portfolio consisting of 60 percent equities and 40 percent high-quality bonds designed to produce attractive returns and avoid steep losses. It is important for associations to revisit their approach to investing and question whether the typical 60/40 portfolio still makes sense.

The stellar return of equities since 1982, despite several bear markets in the interim, played a large role in the 60/40 success story. If there is a “secret sauce” to this formula, however, it lies in the 40 percent invested in high-quality bonds. This may seem counterintuitive since fixed-income returns have not been nearly as impressive as those of equities over that timeframe, yet investors still realized a number of benefits including:

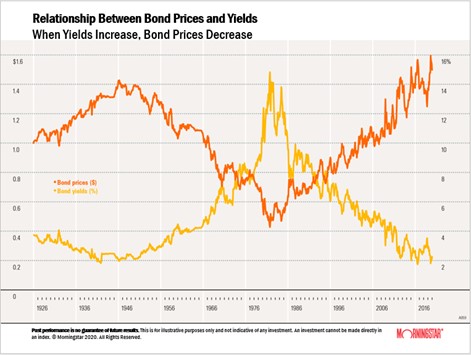

Capital appreciation. Bond prices (orange line in the chart below) and yields (yellow line) move in opposite directions. In 1981, the yield on US government bonds stood just shy of 15 percent. Over the following four decades, yields continued to fall, albeit not in a straight line. The multidecade tailwind provided significant, ongoing support to bond prices. In March of this year, yields even fell below those of the 1930s, marking an 80-year “round trip.” How much higher can bond prices go now that yields are nearing zero?

Income. As stated above, interest income was much higher than it is currently and when combined with price appreciation produced a dependable source of equity-like returns. Further, reinvested interest compounded faster as falling yields led to even higher bond prices.

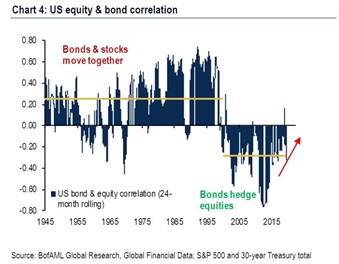

Reduced volatility. For most of the last 20 years, stocks and bonds have been negatively correlated, meaning when stock prices fell, bond prices rose. This was especially helpful during periods of extreme market volatility, such as during the 2008-09 Great Financial Crisis or the COVID-induced bear market earlier this year. However, for much of the post WWII period, stock and bond prices moved in tandem.

The persistence of these long-term tailwinds offered additional benefits to balanced portfolio investors including:

The various economic and political forces that have pushed both short-term interest rates and longer-term government bond yields lower over the last 40 years have been exhausted, or are nearly so. Short-term interest rates are once again at zero percent, and US government bond yields aren’t much higher. In addition, measures adopted by the Federal Reserve in the wake of the COVID pandemic to support the corporate bond market have pushed their yields down to their pre-crisis levels, leading many income-seeking investors to assume greater risk in the search for yield. This is a challenging environment to be sure. So, what should investors do?

Revisit return assumptions. Over the next five to 10 years, equities may produce the same returns they have produced on average over the past five, 10, or 20 years. High-quality bonds likely will not.

Broaden the investment opportunity set. Consider non-bond sources of income and growth, such as preferred stock, convertible bonds, bank loans, real estate, and energy infrastructure. While not a replacement for high-quality fixed income when added to a portfolio in a balanced fashion, they may improve diversification and enhance returns.

Consider a move away from simple passive. In fixed income, there are pros and cons to both a simple, passive approach and an “enhanced” index-based one that tilts away from basic indices to try to unlock other sources of return. It is important to understand the tradeoffs. In the context of this article, the benefit of a passive approach to fixed income is that it offers the prospect of more predictable outcomes (as well as lower fees). However, as discussed throughout this article, the tradeoff is the acceptance of lower expected returns. Moving away from a basic passive approach may produce a wider range of outcomes. However, due to the advancement in the tools available to investors, it offers the possibility of benchmark-beating returns, while maintaining significant cost effectiveness and transparency.

In evaluating today’s interest rate and geopolitical environments, we are reminded of the popular quote from the legendary investor Sir John Templeton: “The four most dangerous words in finance are this time is different.” The 60/40 balanced portfolio has been considered by some to be the gold standard used by associations to measure the relative performance of their reserve portfolios for over a generation. Nonetheless, challenging risk and return assumptions is a time-tested strategy that never goes out of style.

—

The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Any opinions are those of Paul Grambsch and Adam Proger and not necessarily those of Raymond James. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Past performance may not be indicative of future results. Investments mentioned may not be suitable for all investors. Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. There is an inverse relationship between interest rate movements and fixed income prices. Generally, when interest rates rise, fixed income prices fall and when interest rates fall, fixed income prices rise. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Rebalancing a non-retirement account could be a taxable event that may increase your tax liability.