Brian E. Bender

Brian E. Bender, MBA, CPA, CAE, is senior manager and co-chair of the nonprofit practice group at S.R. Snodgrass, P.C., in Cranberry Township, Pennsylvania.

With 2020 being an election year that is also plagued by a global pandemic, more associations are connecting with legislators. However, failure to properly document these interactions and related costs can lead to an array of penalties, even loss of tax-exempt status.

As the 2020 presidential election nears and as the world deals with the COVID-19 crisis, associations are likely engaging with federal, state, and local officials in some way. Although interacting with these officials is not necessarily problematic, failing to meet the required registration and filing requirements can be costly. An inadvertent breakdown in communications between government relations professionals and their finance counterparts can result in inaccurate reporting, noncompliance, additional tax liabilities, or even a loss of tax-exempt status.

Errors in filing and reporting are sometimes caused by the interpretation of the significantly different definitions of lobbying by the IRS and the Lobbying Disclosure Act. Organizations that lobby are required to register under the LDA if at least one of their employees will make more than one lobbying contact and spend more than 20 percent of his or her time on lobbying activities, as defined under the LDA. Registered organizations must submit quarterly reports to Congress about their lobbying activities, including the amount spent on lobbying. State registration requirements and definitions of lobbying differ by state and should be examined on a state-by-state basis.

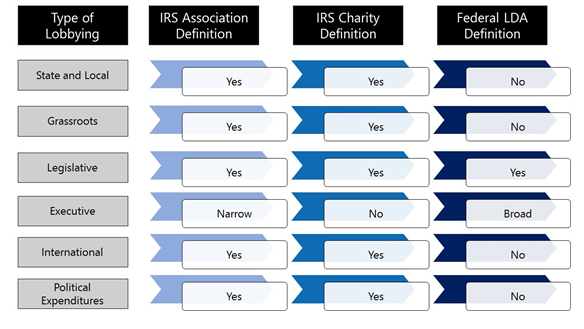

Additionally, every organization, regardless of its LDA registration status, must report annually on its lobbying activities on IRS Form 990. To further complicate matters, the IRS defines lobbying differently for 501(c)(6) associations and 501(c)(3) membership organizations, resulting in three distinctly dissimilar definitions of lobbying. The following chart provides an abbreviated summary of these three definitions:

Regardless of the definition followed, it is important to consider all costs, including, but not limited to salaries, consulting, research tools, publications, travel, meals, entertainment, other reimbursable costs, supporting activities, and membership dues and sponsorships that might be considered lobbying, wholly or in part. The allocable portion of fringe benefits and overhead attributable to internal staff time must also be calculated and included as lobbying expenditures. Certain activities are expressly exempt from the various definitions of lobbying and should be considered very carefully when calculating total costs.

Associations and other taxable business entities are subject to IRS Code Section 162(e), which denies a deduction for and defines lobbying. Associations that incur lobbying costs can choose to notify their members of a reasonable estimate of the portion of the dues allocable to those expenditures for which a deduction is disallowed. An association that does not provide this information to its members must pay a proxy tax on the amount of nondeductible expenditures at the highest corporate rate.

These nonprofits must provide that “no substantial part” of their activities constitute lobbying activities. Exceeding this “substantial part” limit puts an organization at risk of losing its tax-exempt status.

An inadvertent breakdown in communications between government relations professionals and their finance counterparts can result in inaccurate reporting, noncompliance, additional tax liabilities, or even a loss of tax-exempt status.

The substantial part test is very subjective, and the IRS considers a variety of factors when making its determination. Nonprofits that file IRS Form 5768 and make the “lobbying election” under Code Section 501(h) are governed by a separate expenditure test, which includes a mathematical formula that limits the amount an organization can spend on lobbying activities and includes a specific definition for nonprofits to reference that is subject to a maximum overall cap of $1 million in annual lobbying expenditures, of which grassroots lobbying may not exceed 25 percent of the permitted overall lobbying expenditures.

Although all organizations are permitted to engage in lobbying, it is important to understand how they can and cannot participate in or intervene with a political campaign on behalf of or in opposition to a candidate at the local, state, or federal level.

501(c)(3) membership organizations are prohibited from such activities and cannot endorse, make contributions to, or communicate support of or opposition to political candidates. Although political campaign intervention is allowable by 501(c)(6) associations, it may not be its primary activity. 501(c)(6) associations may also make contributions to candidates (if allowable under state law), form a political action committee (PAC) or other 527 political organization, endorse candidates, and communicate support of or opposition to candidates.

Although many organizations are subject to both IRS and LDA reporting requirements, a provision of the LDA permits organizations to track and disclose lobbying expenditures using the applicable IRS definition rather than the LDA definition, which means that only one method would be required to track and report lobbying costs. This is an attractive option to many nonprofits, as tracking lobbying expenses under two different methods increases recordkeeping obligations; however, because state, local, and grassroots lobbying expenses are not included in the LDA definition, organizations sensitive to reporting high-dollar amounts in their LDA reports may consider opting to track lobbying activities separately under both definitions.

To remain compliant and avoid reporting issues, associations and membership organizations should include their government relations department, finance staff, auditors, and attorney in lobbying discussions to work collaboratively. Working together will ensure the appropriate definition(s) are followed and adherence to internal processes and accurate reporting on a quarterly basis. Additionally, associations and membership organizations should consider engaging a professional firm to educate staff and senior leadership to avoid noncompliance.