Dennis Gogarty

Dennis Gogarty, CFP, AIF, is president of Raffa Wealth Management in Washington, DC, and vice chair of ASAE’s Finance and Business Operations Professionals Advisory Council.

The 2016 Study on Nonprofit Investing offers associations and nonprofits insight on various investment practices among their peers, such as decision-making authority, rebalancing policies, and portfolio benchmarking. Get a look at highlights from the study here.

Launched in 2012, the annual Study on Nonprofit Investing (SONI), a joint research project of Raffa Wealth Management LLC and Raffa PC, seeks to meet the need for timely, relevant, actionable data about how nonprofits invest their reserves and how their investments perform.

The 2016 SONI results report has been released with peer benchmarking updates to performance returns and asset allocation through calendar year-end 2015. The report also includes peer statistics for various organizational investment policy considerations, such as decision-making authority, rebalancing policies, and portfolio benchmarking.

Interest in SONI increased substantially in 2016, with 722 nonprofits participating. The results are segmented by nonprofit type and budget size. Among the 193 associations participating, 42 percent identified as trade associations and 28 percent identified as either a professional society or accrediting association. Meanwhile, 47 percent of the associations participating had budgets in excess of $5 million.

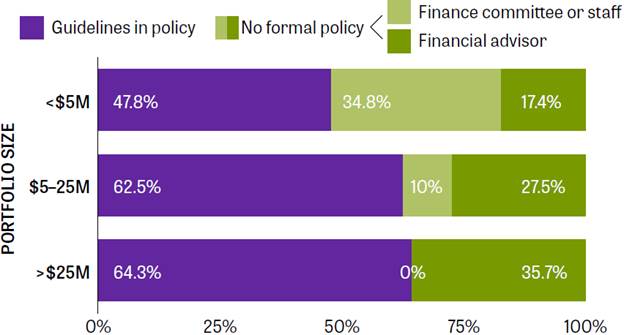

A majority of large associations, but slightly fewer than half of small associations, maintain a formal policy to guide portfolio-rebalancing decisions.

This article outlines select findings from the 2016 SONI Associations results report. Complete details can be found in the full SONI Associations results report.

Association reserves are defined in SONI as total liquid cash assets—or, more specifically, the combined total held in checking accounts, excess operating cash, short- and intermediate-term accounts, and a long-term portfolio or endowment.

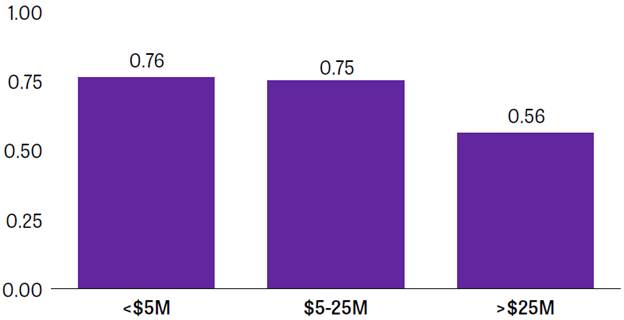

For the two smaller cohorts, the median association reserve-to-budget ratio was 0.75 (or approximately nine months' worth of their annual budget in cash assets). The median in the largest cohort held closer to six to seven months of their budget in reserves.

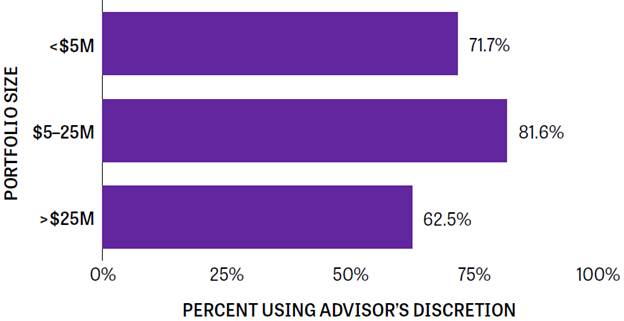

Associations have a choice to either grant discretionary authority to investment advisors to make portfolio changes consistent with the organization's investment policy statement or retain final decision-making authority internally. The majority of those making final decisions internally use advisors to make recommendations.

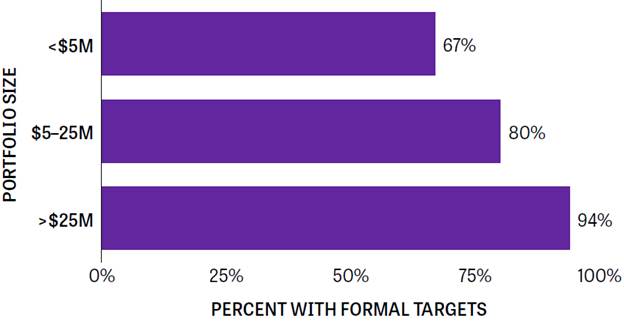

Some associations require investments to be managed at or near specific asset-class allocation targets (for example, 60 percent stocks and 40 percent bonds), while other policies allow more flexibility. The larger the association is, the more likely it is to have formal asset allocation targets.

When it comes to rebalancing, organizations must again decide whether or not guidelines should be outlined in their investment policy or if advisors or volunteer committees should be empowered to make ad-hoc rebalancing judgments. If ad-hoc judgments are allowed, however, organizations must decide if they should be made externally by an investment advisor or internally by staff or committee members.

A majority of large associations, but slightly fewer than half of small associations, maintain a formal policy to guide rebalancing decisions. Among those with no formal policy, a slight majority reported giving authority to a finance committee or staff member to drive rebalancing decisions.

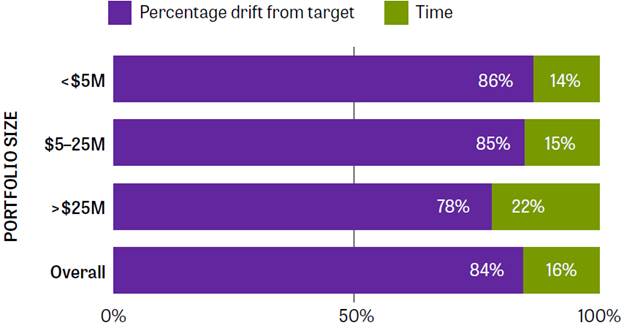

Among those with formal rebalancing policies, a strong majority prefer allowing allocations to drift from targets by a certain percentage, rather than by time, before requiring a rebalance.

In order to assess how nonprofits segment their liquid cash assets, we asked survey participants how much in assets they held in the following four buckets:

We then grouped the first two buckets and the last two buckets together to show the split among total liquid assets held in cash versus those invested for some longer term objective. Associations' segmentation of total liquid assets varied by size, with smaller organizations maintaining more of their liquid assets in cash and larger organizations maintaining a roughly 40/60 split between cash and longer term investments.

Participants were asked what percentage of their long-term reserves should be allocated to stocks, bonds, cash, and alternative investments according to their organization's investment policy targets.

As expected, larger organizations invest more aggressively, allocating more to stock and alternative investments.

The median investment performance for year-end 2015 was negative across all three association size cohorts. Smaller organizations reported slightly better performance than larger organizations. Over the last three years, larger organizations with more growth-oriented investment policies outperformed smaller organizations. This is expected given market conditions that favored stocks to bonds.

The full SONI Associations report (available to ASAE members upon request) details investment returns by association size and target asset allocation policy.

The 2016 SONI report reveals important opportunities for associations to strengthen investment policies and procedures and seek to improve decision making. For example, having a clear target asset allocation policy, with a relatively narrow rebalancing range, helps prevent emotions from driving decisions in the face of market volatility. Including a simple portfolio benchmark to set performance expectations based on policy targets and market conditions allows an organization to be clear about the level of underperformance that is tolerable and improves accountability.

At Raffa Wealth Management, we believe risk and return are directly related. Rather than seeking to circumvent this fundamental relationship, we strongly encourage associations to keep investing simple and act with discipline. In our experience, simple is good when it comes to investing:

For more information about SONI and to download the 2016 SONI Results Executive Summary, visit www.npinvesting.org. Survey participants receive the full report at no cost and active members of ASAE may receive a free copy by sending a request to SONI@raffawealth.com.

All survey and performance results have been compiled solely by Raffa Wealth Management based on information provided by survey respondents. Results have not been independently audited or verified. The views expressed herein are opinions reflecting the best professional judgment of Raffa Wealth Management, LLC. This report is for informational purposes only. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy made reference to directly or indirectly in this report will be profitable or be suitable for your nonprofit's portfolio. Information contained in this article and the SONI reports are not personalized investment advice from Raffa Wealth Management, LLC.